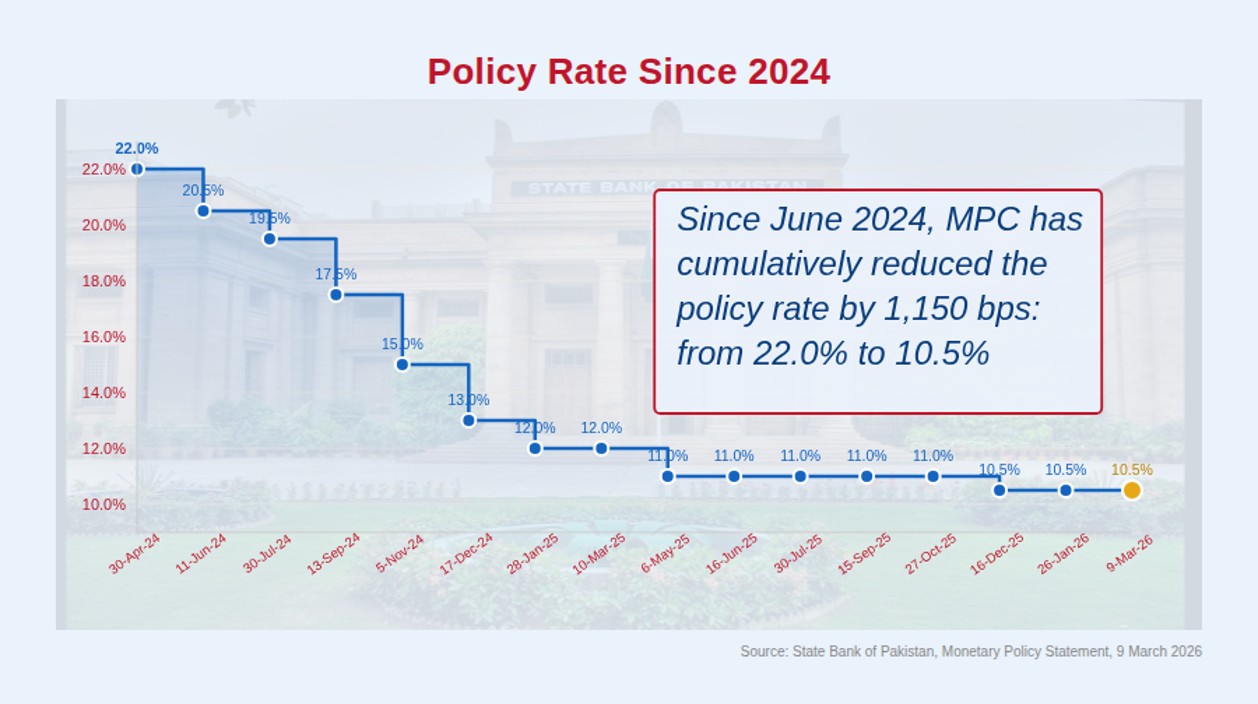

On 9 March 2026, the State Bank of Pakistan (SBP) held its policy rate steady at 10.5%, pausing a cutting cycle that had reduced borrowing costs by 1,150 basis points in less than two years. The Monetary Policy Committee (MPC) cited a sharply deteriorating geopolitical environment following the outbreak of war in the Middle East, which has disrupted global fuel supplies, raised freight and insurance costs, and closed the Strait of Hormuz, as basis for keeping the policy rate unchanged. For millions of Pakistanis with loans, savings accounts, or businesses dependent on credit, the announcement carried immediate consequences, even if the mechanism behind it remains poorly understood. This explainer breaks down the concepts and process behind the process.

What are monetary policy and policy rate?

Monetary policy is the mechanism through which central banks influences interest rates and/or money supply in the economy with the objective to keep overall prices and financial markets stable.

The policy rate is the interest rate at which the SBP lends money to banks and other market participants overnight. When banks borrow at a certain rate from the central bank, they pass that cost on to everyone else. A higher policy rate means banks charge businesses and individuals more to borrow. A lower rate makes borrowing cheaper.

Think of it as the economy’s base price for money. Everything else — home loans, business credit, government debt — is priced around it.

Who sets the policy rate?

Under the State Bank of Pakistan Act, 1956, the Monetary Policy Committee of the SBP is responsible for formulating monetary policy, including decisions on the policy rate. MPC is a 10-member committee comprising:

- SBP Governor or in his absence Deputy Governor nominated by him/her

- Three senior executives of the Bank nominated by SBP Governor

- Three members from SBP Board nominated by the Board

- Three external members including eminent professionals and academics from the fields of economics, finance or banking

After each MPC meeting, the SBP issues a Monetary Policy Statement that provides an assessment of economic conditions and announces its policy decisions.

SBP published an advance calendar of MPC meetings for current financial year 2025-2026 in July last year. The meeting held on March 9, 2026 was the sixth MPC meeting the current year. Two more meetings are scheduled before the end of the fiscal year in June 2026 — the seventh on April 27, 2026 and the eighth on June 15, 2026.

How do policy rate changes affect people?

Changes in the policy rate influence interest rates across the financial system, particularly in the interbank market where banks lend to each other.

A key benchmark in this market is the Karachi Interbank Offered Rate (KIBOR), which is calculated and published daily by the Financial Markets Association of Pakistan for various lending tenors ranging from overnight to one year.

KIBOR is widely used as the reference rate for corporate loans, trade finance, and working capital financing. Banks typically price such loans at KIBOR plus a fixed margin. When KIBOR rises, borrowing becomes more expensive for businesses when their loans are reset.

Although less visible to the public, many consumer financial products — including credit cards and adjustable-rate loans — are also linked to KIBOR. As a result, changes in the policy rate can affect borrowing costs for both businesses and households.

The policy rate affects inflation by influencing borrowing costs, spending, and investment in the economy. When interest rates are low, borrowing becomes cheaper, encouraging consumers to spend and businesses to invest. Higher demand can push prices upward.

When the policy rate increases, borrowing becomes more expensive, which tends to slow spending and investment. Lower demand can help ease pressure on prices.